What is a 1Plus1 Loans CIFAS marker?+

A 1Plus1 Loans CIFAS marker is a fraud-risk record connected to a lending relationship with 1Plus1 Loans, now associated with Credit Labs Limited. It may relate to the loan application, affordability information, Open Banking records, guarantor details, identity checks, or how the loan was obtained or used.

Can a 1Plus1 Loans CIFAS marker be removed?+

Yes. A 1Plus1 Loans CIFAS marker can be removed if the filing cannot be properly justified. The complaint needs to challenge the evidence, the marker category, and whether the marker is accurate, fair, and lawful under data protection principles.

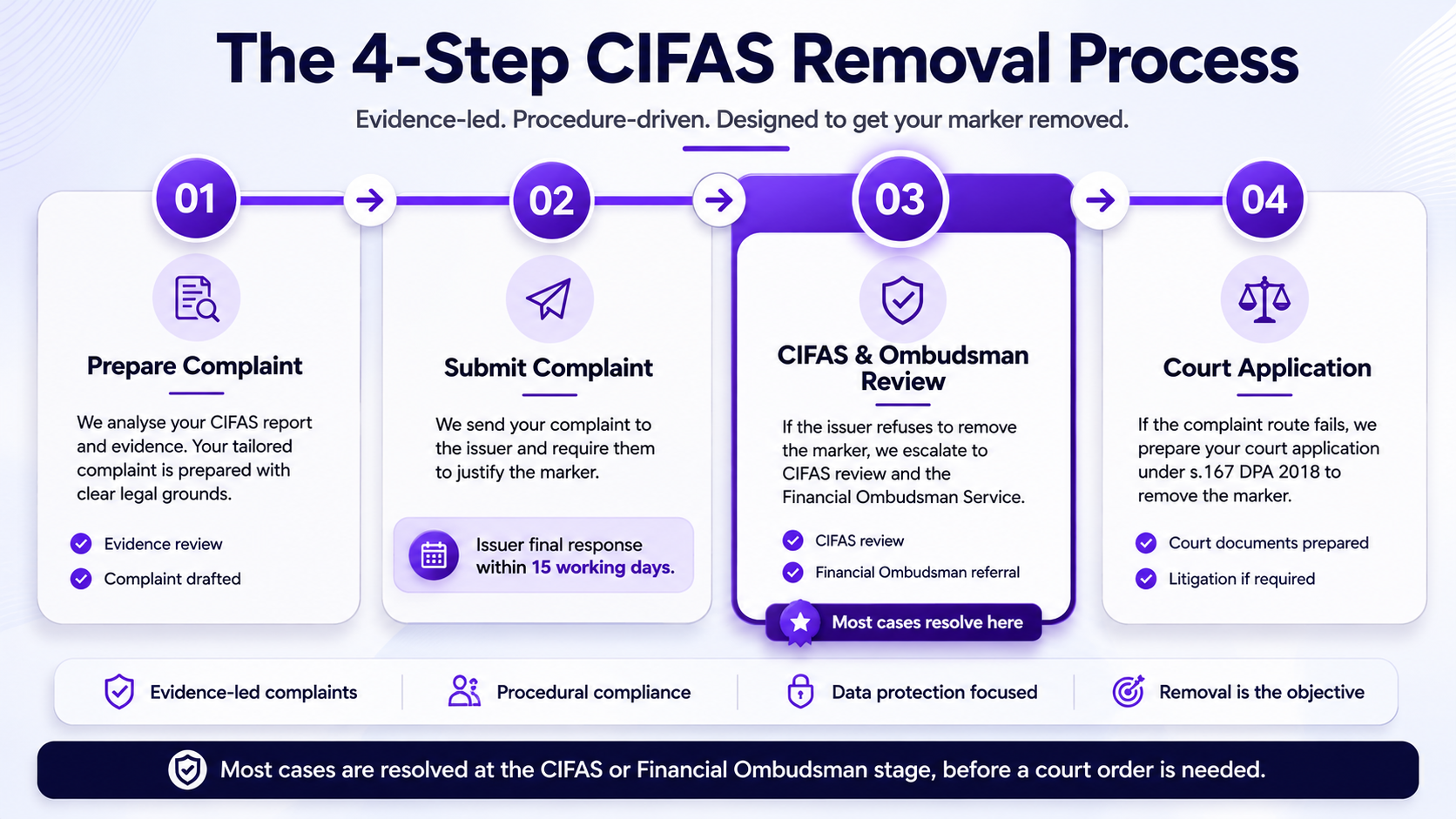

How do I start removing a 1Plus1 Loans CIFAS marker?+

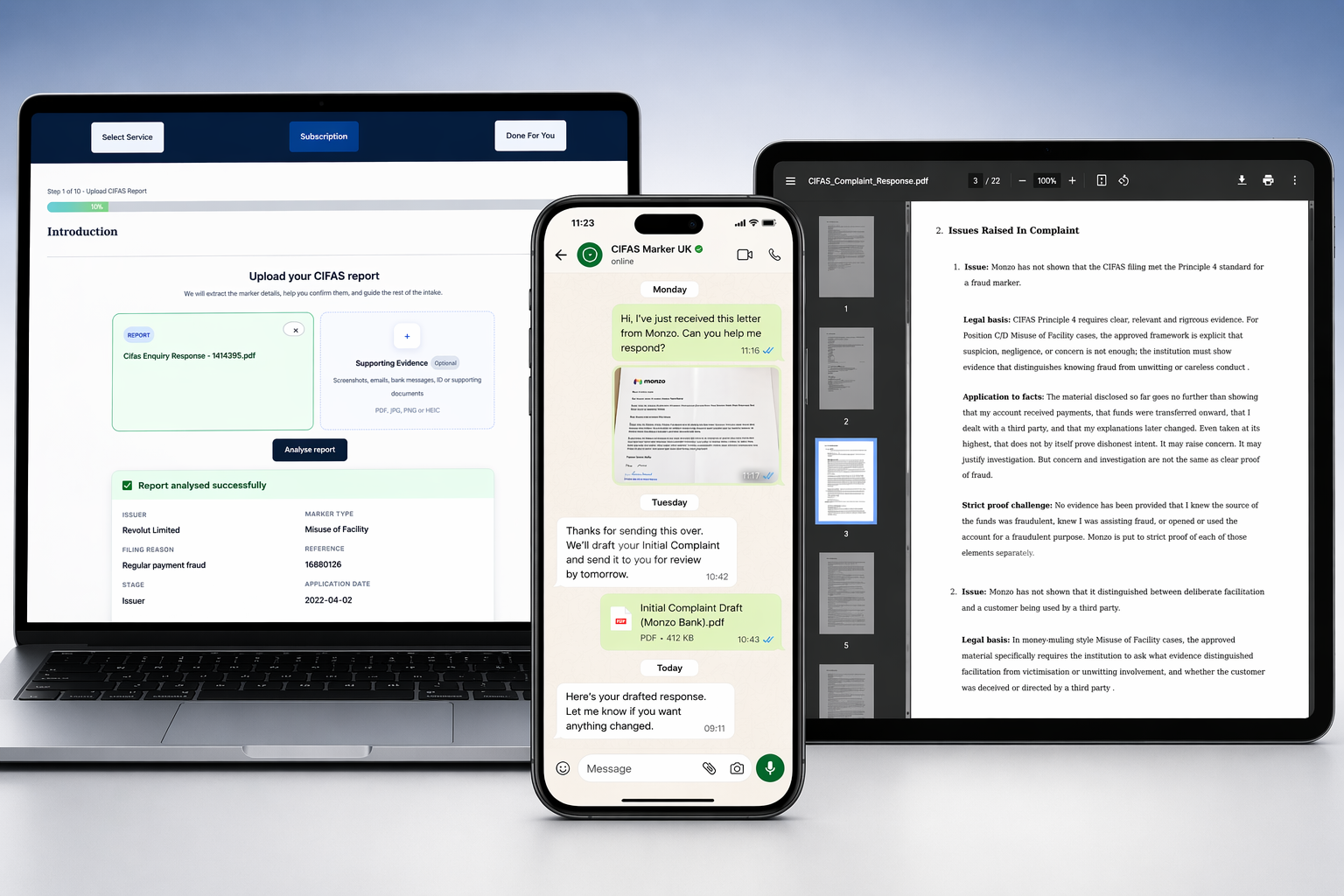

Start by requesting your CIFAS DSAR and gathering any records you have from 1Plus1 Loans. Then upload your CIFAS report, loan documents, emails, screenshots, bank records, guarantor evidence, and a short explanation of what happened so the complaint package can be prepared.

What evidence do I need for a 1Plus1 Loans CIFAS marker complaint?+

Useful evidence may include your CIFAS report, 1Plus1 Loans DSAR response, loan agreement, application records, guarantor documents, bank statements, Open Banking information, emails, messages, fraud reports, account closure letters, refusal letters, and evidence showing the impact of the marker.

How long does 1Plus1 Loans have to respond?+

After the complaint is submitted, 1Plus1 Loans will usually have up to 8 weeks to investigate and issue a Final Response Letter. If no proper final response is received, or if the marker is maintained, the case may be ready for escalation.

What happens if 1Plus1 Loans refuses to remove the marker?+

If 1Plus1 Loans refuses removal, upload the Final Response Letter to your case file. We can then prepare the Financial Ombudsman complaint documents and CIFAS review responses so the matter can be escalated.

Can the Financial Ombudsman remove a 1Plus1 Loans CIFAS marker?+

The Financial Ombudsman Service can require an issuer to remove or correct a marker where it decides the firm acted unfairly or unreasonably. It may also award compensation where appropriate.

Can CIFAS remove a 1Plus1 Loans marker?+

CIFAS can review whether the marker meets the standards required for inclusion on the National Fraud Database. If the filing is not properly justified, CIFAS may require the issuer to amend or remove it.

Do I need to write the complaint letter myself?+

No. Once you upload your CIFAS report, 1Plus1 Loans records, and supporting evidence, we prepare the complaint letter, evidence summary, removal request, and escalation roadmap for you.

Do you take a percentage of compensation?+

No. If compensation is awarded by the Financial Ombudsman Service or another route, it is paid directly to you. We do not charge a success fee and we do not take a percentage of your compensation.